MANAGING YOUR CHAPTER'S FINANCES

A successful chapter operates like a well-run business, particularly when it comes to the finances. Chapters provide educational programs and networking opportunities for local members, and the cost of these services must be properly tracked and summarized annually in the Chapter Financial Report submitted to ACC Headquarters.

Chapters generate revenue from several sources, including ACC rebates, program registration fees, grants, and sponsorships. Like expenses, all income should be carefully monitored, accurately recorded, and used to benefit chapter members.

While the chapter treasurer is responsible for managing these financial matters, the president and board must remain fully informed of the chapter’s financial position. The following section outlines the financial responsibilities of both the chapter and its treasurer.

- ACC Requirements for Chapters: Financial & Legal

- ACC Financial Portal

- ACC Financial Policies Overview (2025 Treasurer Call Slide Deck)

- Chapter Grant Policy (Submissions will open December 2025)

ANNUAL OPERATING BUDGET

A well-prepared annual operating budget is both a tool for evaluating chapter performance and a work plan guiding decisions throughout the year. It allows the chapter to compare current operations with expectations and with previous years’ results.

To create a meaningful budget:

- Each officer with authority to spend or obligate funds should submit a budget proposal to the treasurer 3–5 months before the fiscal year begins. Written notes detailing projected income and expenses should accompany each request.

- The treasurer reviews each proposal for reasonableness and alignment with the chapter’s mission and strategic goals. Comparing proposed amounts to prior-year results (available through the online chapter financial reporting system) helps ensure accuracy.

- The treasurer balances projected expenses against projected income. If expenses exceed income, activities and expenses must be prioritized.

Once the preliminary budget is established (before October 1), the treasurer presents the balanced budget to the Board for approval. After approval, integrate the budget into the financial statement cycle, using it to guide activities throughout the year.

As part of the chapter's annual obligations, the treasurer must submit the approved budget along with the annual financial report (due in November), to ACC Headquarters via the Financial Reporting Portal.

ANNUAL CHAPTER FINANCIAL REPORT

All chapters are required to submit their Chapter Financial Report through the Financial Reporting Portal in November. Completing this report is critical because ACC HQ files the association’s federal tax returns on behalf of all chapters.

Failure to provide a complete and timely report can result in:

- IRS penalties and interest for the association

- Additional accountant fees

- Withholding of quarterly rebate payments until proper and accurate financial information is submitted

Full cooperation from every chapter is essential to ensure compliance and avoid unnecessary costs.

FY25 Financial Reporting Overview

CHAPTER RESERVE POLICY

ACC advises chapters to maintain reserves equal to 3-6 months of operating expenses.

- Chapters with 6–9 months of reserves are encouraged to use excess funds to enhance programming, support member activities, and raise the chapter’s visibility in the local community.

- Chapters with reserves exceeding 9 months may see an impact on their rebates, and the financial reporting process now requires a written explanation for excess funds.

Reserve levels can influence how both members and ACC Headquarters perceive a chapter's fiscal responsibility and management. For example, members may be hesitant to support a dues increase if their chapter:

- Fails to meet current member needs

- Lacks plans to invest funds in future member services

- Is holding excessive reserves without clear purpose

To avoid such situations, chapters should allocate surplus funds beyond the recommended 6-month threshold towards improving chapter services. Specific recommendations for using excess income are provided below:

- Fund one or more chapter board representatives to attend the ACC Leadership Development Institute (chapter leader training) sessions in the spring and fall.

- Provide your chapter administrator with training related to their duties – technical, event management, business writing, membership development, etc., and support their participation in ACC Admin Training Day, a dedicated annual 1-day event in October to exchange ideas and learn from peers.

- Contract a professional bookkeeper to relieve either the volunteer treasurer or paid administrator of this day-to-day responsibility. This will increase overall financial controls by segregating duties; however, the treasurer should continue to provide oversight.

- Hire an event management company for large chapter events, to relieve volunteers of the day-to-day operations.

- Hire a PR firm to assist with marketing your chapter to your local legal community.

- Hire a professional photographer for higher-profile events.

- Conduct local member recruitment campaigns and/or drives. For advice and direction on hosting a local incentive campaign, email chapters@acc.com.

- Fund a unique program without sponsor involvement (a CLO networking event, social event, etc.)

- Purchase chapter letterhead and business cards.

- Hire experts such as executive coaches, resume writing experts, etc. to assist members in transition and members who are interested in moving to the next level.

- Fund unique speakers for one or more of your events.

- Fund an internship program or scholarship program for law students.

RESERVE LIMITS

Chapters often wonder if the IRS places limits on the reserves a chapter is allowed to hold. In fact, the IRS does not focus on a tax-exempt organization reserve, as long as the use of the reserves is to ultimately carry out the objectives the organization was granted tax-exempt status and there is not a gross excess of funds not being spent on chapter services. (A large reserve fund may be justified, for example, if the chapter plans to set up a scholarship program, produce a directory, or host a large annual event). Note, however, reserves, which remain at levels higher than the recommended 6-9 months operating expenses, could cause undue scrutiny by the IRS. Chapters should therefore endeavor to continually use excess funds to enhance chapters services and operations.

ACCOUNTING METHOD & RECORD KEEPING

All chapters should operate on a cash basis. This means income and expenses are recognized when they occur (receipt of a check or payment of a bill), as opposed to when they are due. ACC recommends your chapter’s accounting system be as simple as possible yet still meet the annual ACC Headquarters reporting requirements. If, however, the chapter wishes to maintain a more detailed, accrual accounting system, you may do so as long as you submit your annual on a cash basis.

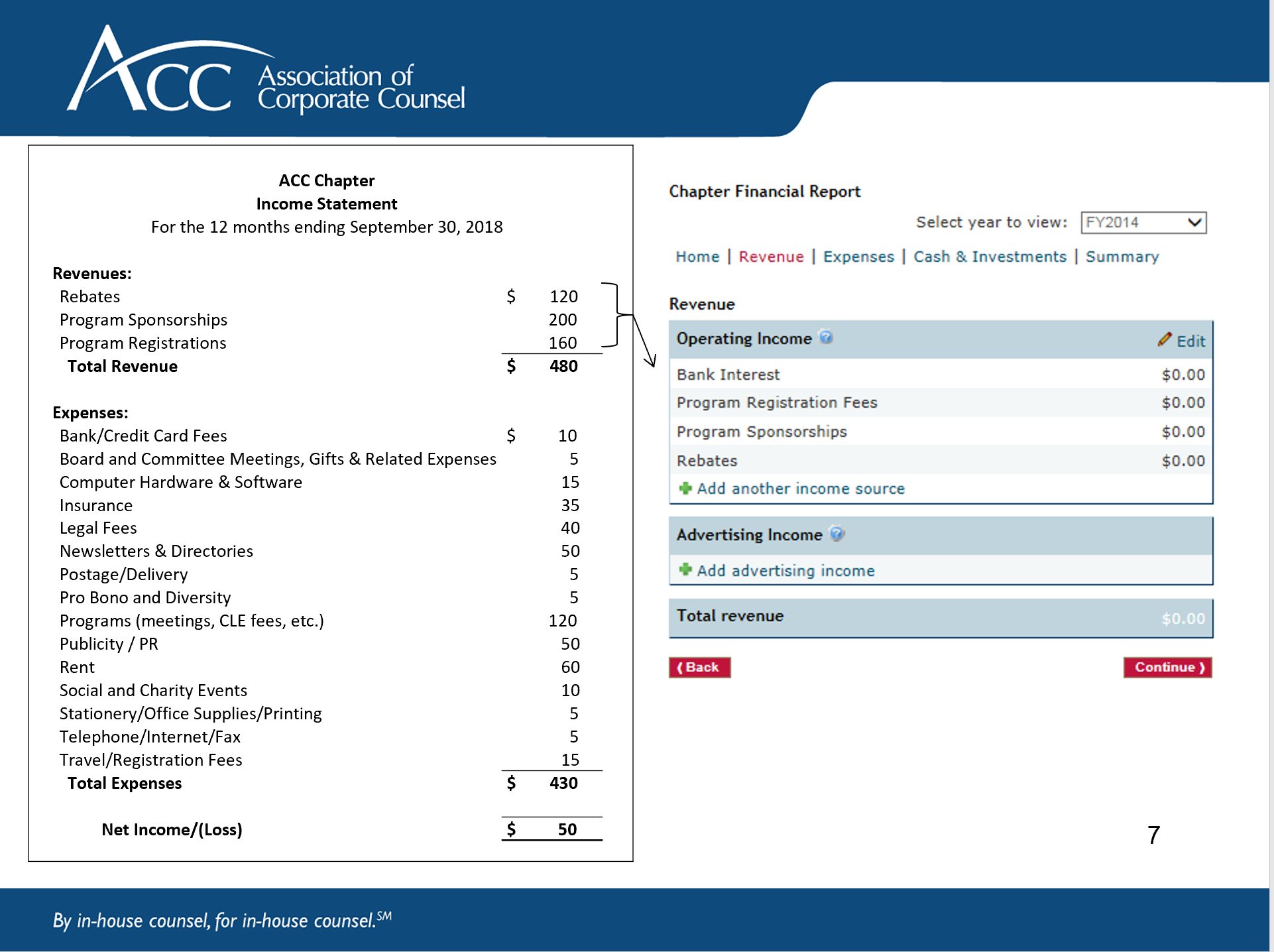

As demonstrated in the attached copy of the annual Chapter Financial Report, ACC Headquarters requires the distribution of income and expenses between logical and common categories. Each Chapter should be able to produce a standard Profit and Loss Statement and Balance Sheet quarterly, if not monthly.

When choosing or setting up an accounting system, it’s important to ensure it can be easily transferred to a new treasurer at the end of each term. Look for a system that is simple to use, well-documented, and not overly complex. QuickBooks is a commonly used option that meets these needs and also offers a hosted online version, which makes it easy for a treasurer to monitor accounts remotely.

INTERNAL CONTROLS

Each chapter is required to adopt accounting procedures that include strong internal controls, with the separation of duties as their foundation. Since many chapters have only one administrator, full separation may not be possible. In these cases, the treasurer must take an active role in overseeing chapter funds. If the treasurer also serves as the bookkeeper, another officer should provide oversight to maintain proper checks and balances. In addition, chapters should establish an audit committee, as typically outlined in their bylaws, to provide independent oversight of financial practices and strengthen accountability. Whenever possible, include volunteers with audit, finance, or accounting experience.

Sample Chapter Financial Controls Policy (ACC HQ 2025).

Sample of Audit Committee Volunteer Assistance.

CASH, CREDIT CARDS AND INVESTMENTS

CASH

- To reduce loss of funds, minimize all cash transactions.

- Use an online event registration system that accepts credit card payments, for all programs.

- If cash is received, issue a cash receipt for all transactions.

BANK DEPOSITS

- Endorse checks “For deposit only” upon receipt and require the deposit of all inbound checks be made to the bank every two weeks.

PETTY CASH

- Allow administrator to keep a petty cash fund (approximately $250) in a locked bank box to pay for small, non-reoccurring expenses such as taxis, office supplies, etc.

- Reimbursement is made as needed with a check payable to administrator.

WIRE TRANSFERS

- Allow only the treasurer the right to electronically transfer funds out of account.

INVESTMENTS

- Establish an investment policy for the chapter. View an example here.

- Conduct quarterly or semi-annual reviews of the investments with investment manager.

- Allow only the treasurer, with Board approval, the authority to purchase or liquidate an investment.

BANK RECONCILIATION

- Ensure a proper bank reconciliation is conducted every month.

- Treasurers should review and initial reconciliations every six months.

CREDIT CARDS

- Accept only the three major credit cards as payment.

- Have net proceeds deposited directly into a FDIC bank account.

- Store credit card information in a secure location. If credit card payment is stored electronically, ensure the safety of such information against third-party access.

- Ensure credit card processors do not allow a credit to be issued to a card that has never been charged.

ACCOUNTS PAYABLE

INVOICES

- All invoices should be date-stamped upon receipt.

- Attach proof of services rendered to invoice: copy of contract, sample of printed matter, copy of flyer for program, etc.

CHECKS

- Ensure checks are maintained in a secure location.

- Never make any check payable to cash and never sign a blank check.

- Require two signatures for all checks over a reasonable limit ($5,000 or more).

- Do not allow administrator to sign their compensation.

- Pay from original invoices only. Fax copies can easily be altered.

- Have the treasurer review a list of all checks monthly or quarterly. List should contain name of payee, date, amount and explanation of expense.

CODE TO CHART OF ACCOUNTS

- Code income and expenses to the proper categories, which may be different than where it was budgeted. Consistent coding allows for proper historical comparisons. For example, if you budget $15,000 for program expenses, but you spend funds in excess of that amount, do not code the additional expenses to a different line item. Instead code the total expenses to programs, so that your expenses represent a true reflection of activities for the year.

ACCOUNTS RECEIVABLE

BAD DEBT AND COLLECTIONS

- To avoid bad debt, to the extent possible, require all sponsorships to be 100% pre-paid prior to an event.

- Maintain an accurate and detailed list of all monies due the chapter. The list should include amount, due date, payee name and address, contact name and number.

- Issue reminder notices or calls for all accounts past due beyond 30 days.

- Ask treasurer or other officer to call accounts past due beyond 60 days.

- Report any non-payment to ACC HQ to assist with collection and/or cease other ACC business with company.

FINANCIAL STATEMENTS

A Treasurer’s Report should be part of each chapter board meeting. That report should contain, at a minimum, a Profit and Loss Statement (P & L) and a Balance Sheet. The P&L statement should compare year-to-date income and expenses against the current budget as well as against last year’s income and expenses. A P&L of this nature will allow a chapter board to fully examine the chapter’s current financial position relative to their budget and the prior year’s actual experience.

A sample format for a financial statement is attached.

{kind=link}

ACC RESERVES THE RIGHT TO INSPECT THE BOOKS OF ANY CHAPTER AT ANY TIME.

INCORPORATION

To provide added protection for chapter directors and officers, ACC has incorporated all of its chapters. For US-based chapters, ACC also manages annual reporting requirements.

Because chapter bylaws must include certain provisions, it is essential that any proposed amendments or revisions are reviewed by ACC staff before they are approved. Please forward all proposed bylaw changes to chapters@acc.com, and ACC staff will coordinate with the Office of the General Counsel.

Benefits of Incorporation:

- Officers and directors are generally not personally liable for chapter-related damages, including personal injury, property damage, or contractual obligations, as long as they act reasonably, prudently, and in good faith. While ACC provides insurance coverage for officers and directors, incorporation adds an extra layer of protection.

- Incorporated chapters can sue or be sued in their own legal name. Unincorporated chapters must rely on individual board members to appear in court.

- Obtaining insurance is easier.

- Each chapter has its own legal identity under ACC, which also helps protect against tax liability.

- If a chapter merges or splits, the process is safer and more clearly defined.

EIN NUMBERS

All chapters are automatically covered under ACC's §501(c)(6) group tax exemption, but each chapter has its own Employer Identification Number (EIN). Chapter members or local sponsors often request the chapter’s EIN for tax purposes, either before or after making a payment. Requests may be verbal, written or submitted via a W-9 form. Chapters should respond promptly to all requests. Include the chapter administrator's address on the form; if no chapter administrator is listed, use the chapter president's address. Always provide the chapter’s EIN, not the EIN of the entire association. ACC Headquarters applies for EIN numbers on behalf of new chapters. Click here to view the chapters' EIN.

TAXES

ACC is a §501(c)(6) not-for-profit organization, which means it is generally exempt from federal and state income taxes in all states and countries to date. However, unrelated business income - such as advertising sales in the US - may be taxable and requires prior approval from ACC HQ before the activity is undertaken. If ACC must pay unrelated business income tax (UBIT) on behalf of a US chapter, the cost may be charged back to the chapter.

Being a non-profit corporation does NOT automatically mean a chapter is exempt from US state sales and use tax. ACC HQ has applied for - and been denied – sales and use tax exemption from District of Columbia several times. Depending on state law, a chapter may have better success with its own application, but §501(c)(6) organizations are generally not granted exemptions. Please contact your local authorities for guidance.

Chapters are not required to file US state income tax returns. ACC HQ files a single federal tax return on behalf of all chapters. If a chapter is contacted by IRS, ACC HQ must be notified promptly and will handle the inquiry on the chapter’s behalf.

The only tax forms a US chapter may need to prepare are:

- 1099-MISC – if the chapter hires an administrator or other consultant as an independent contractor.

- W-2 – if the chapter has an employee.

See the section below for more information on this requirement.

TAX EXEMPT STATUS REVOCATION

Chapters should be aware that a tax-exempt organization can lose its status if any of its net earnings benefit a private individual. This is called inurement. Examples include:

- Rebates to members.

- Dividends to members.

- Executive compensation or benefits in excess of fair market value.

To avoid compensating your administrator above fair market value, contact ACC Headquarters for benchmarking compensation information from other ACC chapters and the American Society of Association Executives (ASAE). We also recommend reaching out to local Association Management Companies to obtain competing bids for the services you need. Even if you do not hire an association management firm, these bids can help you determine a reasonable pay range for an individual performing the same work. - Transactions with officers, directors, or other insiders that are not at fair market value or on standard commercial terms

Example: Michael Johnson, who serves on a chapter’s board of directors, owns 25 percent of Wordsmith Publishing Company. The chapter enters into a contract with Wordsmith Publishing Company to produce its membership directory. Johnson knows this project represents good business for the publishing company; he also knows that, if the chapter inquired, it could print its membership directory for the same quality, but for a lower price at ASAP Publishing Company.

To ensure that you don’t find yourself in this situation, a chapter must create a conflict-of-interest policy. Click here.

CHAPTER EMPLOYEES VS. CONSULTANTS

Many chapters need to hire an administrator to help with the day-to-day operations. The IRS provides a set of questions to determine whether a worker is an independent contractor or an employee. In general, answering “no” to questions 1 through 14 and “yes” to questions 15 through 19 indicates that the worker is an independent contractor.

- Are instructions furnished regarding where, when, and how worker performs?

- Is training required by the employer?

- Is the worker a necessary and vital part of the continuing business operations?

- Are services rendered personally by the worker?

- Is hiring, supervising, and paying of assistance done by the employer?

- Are hours of work set by the employer?

- Does a continuing relationship exist with the employer?

- Is full-time service required by the employer?

- Is the work done on the employer’s premises?

- Is the order or sequence of services set by the employer?

- Are oral or written reports required by the employer?

- Are regular payments (hourly, weekly, monthly) made by the employer?

- Are the worker’s expenses paid by the employer?

- Does the employer have the right to hire and fire the worker?

- Is there a profit or loss possibility by the worker?

- Does the worker have a significant equipment investment?

- Does the worker perform services for more than one organization simultaneously?

- Are the worker’s services available to the general public?

- Is the worker legally obligated to satisfactorily complete the job?

1099 FORMS

US chapter 1099 filing requirements:

- By January 31: Chapters must provide a 1099-NEC to all independent (unincorporated) contractors they worked with during the previous tax year (January 1–December 31). This typically includes chapter administrators, executive directors, and interns. The 1099-NEC is legally required and serves as an alternative to a W-2. Only report fees paid to the contractor, do not include reimbursed expenses.

- By January 31: Chapters must submit all 1099 forms to the IRS:

- 1099-NEC for individuals, contractors, and administrators

- 1099-MISC for rents or attorney fees

- 1096 Form: Chapters must also file a 1096 transmittal form with the IRS, even if only one 1099-NEC is issued.

- ACC Copy: Chapters must send a copy of all issued 1099s to ACC Headquarters at ar@acc.com.

To order 1099 forms online, visit the IRS website, or use a small-business filing service, such as https://quickbooks.intuit.com/payroll/. More information is available at www.irs.gov.

If the 1099 is prepared by the chapter administrator, it should be reviewed by the treasurer or other appropriate board member.

Additionally, chapters should request a W-9 form from any individual or organization receiving a scholarship or contribution. This information is required in the annual Chapter Financial Report and should be collected at the time of payment.

DONATIONS AND SCHOLARSHIPS

Chapters are encouraged to create a charitable giving policy that defines the types of organizations they support and the typical donation amounts. This helps ensure funds are distributed appropriately and promotes strong financial stewardship. View an example here.

Chapters are required to collect the following information for all donations and scholarships:

- Scholarships: recipient’s name, address, and Social Security Number (SSN)

- Donations: recipient’s name, address, Employer Identification Number (EIN), and the IRS code (a numerical/alphabetical designation that identifies the type of organization)

Including this information is mandatory for all donations and scholarships reported in the annual Chapter Financial Report.

REBATE TRANSFERS FROM ACC

All ACC chapters are eligible for membership rebates based on the following criteria:

- Individual members: US$30 for each new or renewing member in the individual category within the chapter’s service region.

- Corporate/corporate premium members: US$15 for each new or renewing member in this category within the chapter’s service region.

- Exclusions: Discounted memberships, including special promotions, Tier B, C, or D in-house counsel memberships, as well as complimentary, retired, or in-transition memberships, do not qualify.

Rebates are calculated based on the receipt of dues payments by ACC for new and renewing members and are typically paid quarterly.

Payment Process:

- ACC sends rebate payments via ACH (for US chapters) or wire transfer (for non-U.S. chapters) to the chapter’s bank account on file.

- Payments may also include small miscellaneous additions or deductions for chapter expenses, such as Zoom fees, quarterly newsletters, or overnight mail charges.

- A detailed rebate memo outlining amounts and deductions is sent to the chapter treasurer (or designee) and administrator with each payment.

Important Requirements:

- Rebates will be withheld if a chapter has not submitted its annual financial report and current fiscal year budget.

- Any withheld rebate becomes void three months after the deadline for the required report.

- Chapters will be notified if a rebate payment is returned. Amounts outstanding for six months will be canceled and cannot be reissued.

INSURANCE

General Liability for U.S. and Canadian Chapters

ACC maintains a general liability insurance policy for all US and Canadian chapters. The primary policy covers incidents such as slip-and-fall accidents and provides host liquor liability protection, with limits of US$1,000,000 per occurrence/US$2,000,000 per policy year. ACC also carries an umbrella policy for US and Canadian chapters with a coverage limit of US$9,000,000.

When US chapters host events involving external vendors – such as hotels, caterers, members' companies, transportation providers or museums - third party may request a Certificate of Insurance (COI). To obtain a COI, submit a fully executed copy of the vendor contract to ACC HQ. Certificates are typically processed within five (5) working days.

Any potential claims must be reported immediately to ACC HQ.

ACC Chapter Insurance Policies:

- General Liability Policy: CNA - Policy # 7014870879 - $1,000,000 per occurrence/$2,000,000 aggregate limit

- Liquor Liability Policy: CNA - Policy # 7014870882 - $1,000,000 per common cause/$2,000,000 aggregate limit

- Umbrella Policy: CNA - Policy # 7014871336 - $9,000,000 per incident/$9,000,000 aggregate limit

GENERAL LIABILITY FOR NON-U.S. AND NON-CANADIAN CHAPTERS

ACC maintains a special general liability insurance policy for all non-US chapters. This policy covers incidents such as slip-and-fall accidents and provides host liquor liability protection with limits of US$1,000,000 per occurrence/US$2,000,000 per policy year. It also includes employer liability, property in-transit coverage, EDP coverage and additional protections. An umbrella policy for non-US chapters provides coverage of US$9,000,000.

When non-US chapters host events with external vendors – such as hotels, caterers, members' companies, transportation providers, or museums – third parties may request a Certificate of Insurance (COI). To obtain a COI, submit a fully executed copy of the vendor contract to ACC HQ. Certificates are typically processed within five (5) working days.

Any potential claims, must be reported immediately to ACC HQ

ACC Chapter Insurance Policies:

- Commercial Package Policy: CNA - Policy # WP 67 329 8905 – Liability – US$1,000,000 per occurrence/US$2,000,000 aggregate limit

- Umbrella Policy: CNA Policy # 7014871336 – US$9,000,000M per incident/ US$9,000,000 aggregate limit

DIRECTORS AND OFFICERS’ LIABILITY POLICY FOR ALL ACC VOLUNTEER LEADERS AND INSURANCE REQUIREMENTS FOR ADMINISTRATORS

ACC maintains a US$10,000,000 Directors’ and Officers’ (D&O) liability insurance policy that covers all ACC volunteer leaders.

- Coverage Exclusions: The policy does not cover chapter administrators or executive directors hired as paid independent consultants. Chapters must require these administrators to carry professional liability insurance, if applicable, and provide proof of coverage within 30 days of contract signing or renewal. Administrators should consult an insurance professional to assess their individual risk and determine appropriate coverage.

- Employee Administrators:

- If hired through an employment agency, the agency must provide workers’ compensation insurance.

- If hired directly by the chapter, the chapter is responsible for complying with all local and national employment laws, including providing workers’ compensation insurance.

- Deductible Reimbursement: ACC may reimburse covered individuals for the D&O policy deductible if the chapter does not have sufficient funds.

Below is the policy information and FAQs. For further questions, contact ACC Headquarters.

- Directors & Officers Policy: CNA - Policy # 268118327 - US$5,000,000; Deductible: US$50,000

- Excess Directors & Officers Policy: Allied World - Policy #0313-8290 - US$5,000,000

DIRECTOR AND OFFICERS' LIABILITY POLICY FAQ'S

-

Who is covered?

The policy covers directors and officers of the organization and its subsidiaries. It provide protection not only for the organization but also for the individual who manage it.Board members and officers can have personal liability for certain actions, and personal assets could be at risk in the event of an adverse judgment.

The policy also covers the costs of defending both the individual(s) and the organization against covered "wrongful acts."

- What is covered?

The policy covers wrongful acts committed by a covered individual or group while performing their duties for the organization.

A wrongful act is an:

A. Act

B. Error

C. Omission

D. Misstatement or misleading statement

E. Neglect or breach of duty

Examples of wrongful acts:

A. Management of funds (not benefit plans)

B. Management of the affairs of the organization

C. Employment practices

D. Publisher's liability (limited to copyright infringement, libel and plagiarism)

E. Libel, slander, or defamation

Examples of what is not covered

A. Bodily injury or property damage

B. Ensured gaining profit or advantage not legally entitled to

C. Willful violation of a statute

D. Fiduciary liability as regards employee benefit or pension plans

E. Failure to maintain insurance

CRIME INSURANCE

ACC’s Crime Insurance protects chapters against dishonesty, fraud, embezzlement, and other wrongful acts by employees, independent consultants and volunteer leaders.

- Crime Policy: Travelers - Policy # 105557058, US$100,000; Retention: US$1,000

This coverage is not included in the umbrella policy. Chapters are responsible for the US$121 annual premium, which will be deducted from the chapter rebates.

MALPRACTICE INSURANCE FOR PRO BONO ACTIVITIES

Chapters that want malpractice insurance, to cover members participating in pro bono work, can purchase coverage through The National Legal Aid and Defender Association (NLADA) at affordable rates. For more information, contact NLADA by phone at + 1 202.452.0620 or email at info@nlada.org.

ONLINE AND PRINT AD INCOME COMPUTATION

Some ACC chapters include online or print ad space to sponsors as part of their sponsorship packages. If these ads are corporate identity ads (see Unrelated Business Income Tax for details), the revenue they generate is taxable and must be reported separately on the Annual Financial Report.

The IRS does not allow taxable income, such as advertising revenue, to be included under a non-taxable category like sponsorships. Therefore, if advertising is included in a sponsorship package, the advertising portion must be calculated separately and be reported as taxable income.

Calculating ONLINE ADVERTISING INCOMe as part of larger sponsorship package

Using ACC’s own market rate for online homepage advertising as a basis, the following formula can be used to compute your chapter’s online advertising income.

Actual monthly price of ACC banner ad: $7,000

Number of ACC members as of 9/30/23: 46,500

Price per ACC member per month: $7,000/46,500 = $.15

Nevertheless, adjustments are required for this formula as chapter homepages cater to a more limited audience. To implement this formula for a chapter, follow these steps:

Price to reach one ACC member per month: $.15

Number of chapter members as of September 30: A

Number of months ad appeared: B

Income per ad formula: $.15 x A x B

To illustrate this formula, assume a chapter had 1,200 members on September 30 and displayed one banner ad per month.

Actual monthly price to reach an ACC member: $.15

Number of chapter members as of September 30: 1,200

Number of months ad appeared: 3

$.15 x 1,200 x 1 = $180.00 Advertising income per month

$180 x 12 = $2,160.00 Total advertising income for the year

Calculating PRINT ADVERTISING INCOME as part of larger Sponsorship Package

Based on ACC's internal market rate for ACC Docket (when it was printed), you can calculate your chapter's print advertising income using the following formula:

ACC Docket is an 8x11 publication printed 10 times per year

Per issue price of a black & white ad: Full page (8x11) - $5,250, Half page (8x5.5) $3,885

ACC Docket circulation: 42,000

Cost per subscriber: Full page = $.13 or $5,250/42,000, Half page = $.09 or $3,885/42,000

The ACC Docket does not sell quarter-page ads.

To apply this formula to a chapter, proceed using the following example:

September 30 membership or circulation of chapter publication – if they differ, use the larger of the two: 400

Size of overall publication: 8x10 newsletter or directory

Size of ad: Full page (8x10), half (8x5)

Price of one full-page ad: 400 x $.13 = $52

Price of one half-page ad: 400 x$.09 = $36

NOTES

- If you run quarter-page ads, given the half-page price is 73% of the full page price, consider making the quarter-page price 73% of the half-page price. The theory is there is better value is in the full page ad and advertisers will upgrade to full.

- The type of publication is not important. If your publication is substantially smaller than 8x11, then decrease the pricing accordingly, as the exposure/ad size will be that much less. So if your publication is 5x7, use the ACC Docket half-page advertising for a full-page ad in this smaller publication.

- If the ad is thanking or congratulating the chapter, it does not need to be included in this calculation.

If you have any questions, please contact ACC Finance.

FINANCIAL AND OPERATIONAL REVIEWS

ACC does not require chapters to have an independent audit, but chapters with income or budgets approaching $500,000 are encouraged to conduct a financial review every 2-3 years. A financial review is less comprehensive and less expensive than a full audit, yet it helps the board meet its financial oversight and governance responsibilities.

Chapters may hire local accountants at their own expense, or request an on-site review by ACC HQ staff at no cost.

An operational review by ACC staff provides a comprehensive evaluation of chapter operations, which many chapters have found highly beneficial. An overview of such a review is provided below:

OVERVIEW OF A CHAPTER OPERATIONS REVIEW BY STAFF FROM ACC HQ

Purpose: The review ensures that an ACC chapter’s financial affairs are managed efficiently and effectively, that funds are properly accounted for, financial controls are in place, the chapter board fulfills its fiduciary duties, and that the chapter operates in compliance with its non-profit status.

Review process:

- The review typically takes 1.5 days and is conducted primarily with the individual who manages the books (administrator, accountant, or volunteer treasurer).

- It is held at the office or location where financial records are maintained.

- Most of the time is spent interviewing the administrator/bookkeeper/treasurer about processes, controls, banking, contracts, and related procedures

Review report:

- An oral summary is provided to the chapter president, treasurer, and relevant board members at the conclusion of the review whenever possible.

- A detailed written report is delivered within 3–6 weeks.

- Chapters are required to submit a written response to the report within three months of receipt.

RECORDS RETENTION POLICY

Chapters should retain monthly and quarterly financial reports, program-specific P&L statements, credit card records, and bank statements for five years from the date of the record or event. For guidance on retaining other types of documents, refer to the full Record Retention Policy.